Published on August 19, 2020

By: Alexander Cochis, Project Manager and Javier Sola, Consultant

Environmental advocates are challenging whether it makes sense to continue with existing pipe replacement programs, arguing that the industry is investing in rate base that will be stranded long before it is fully depreciated.

Key Considerations

- Should a gas company continue, accelerate, or reprioritize its pipe replacement program?

- If regulators place shareholders at risk for new pipe investment, how can local gas distribution companies (LDCs) manage that risk?

- Should the company propose a change to depreciation rates for existing or new pipe?

A pipe replacement framework that incorporates uncertainty attributable to:

- Decarbonization policy

- The economics of electrification

- Customer decisions to continue to use natural gas

Will meet the challenges of a changing environment.

A New Investment Framework

The existing pipe replacement decision-making process focuses on how fast LDCs can replace at-risk pipe and how best to prioritize and execute their pipe replacement programs. These decisions are driven by federal mandates and subject to oversight by state utility regulators that are concerned about safety and cost. Environmental advocates are opposing new pipelines but also suggesting that LDCs should be at risk for future pipe replacement investments, as they increasingly focus on gas planning processes and decisions. Regulators recognize that pipeline safety is paramount. How can LDCs adjust the decision-making framework to support pipe replacement decisions? Our current assessment is that the degree of policy change, technological advances, and the costs of alternatives or substitutes to natural gas all play a role in framing a response to the challenges of decarbonization on pipe investment decisions.

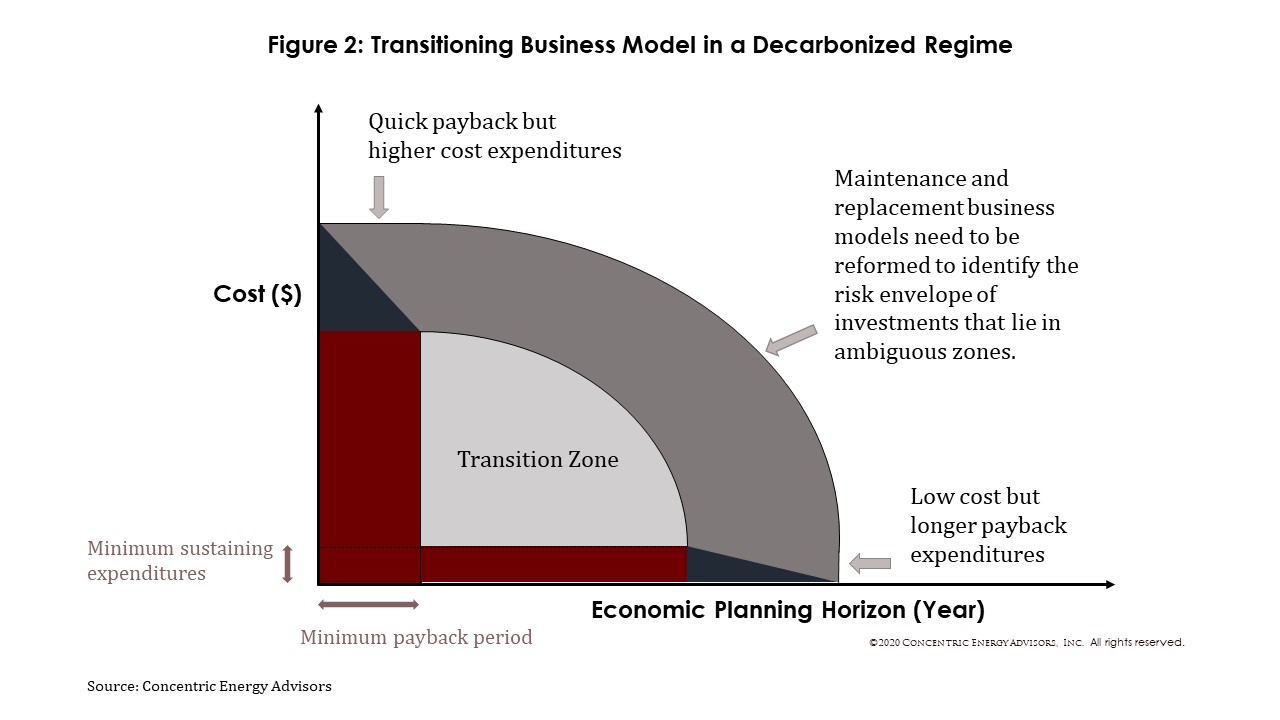

For a gas company to fulfill its public service mandate, it will make ongoing maintenance, monitoring, and operating expenditures to sustain the system and comply with safe operating practices (Figure 1). The LDC can also make investments to grow. As costs increase, operators will decide how long before those outlays are completely recovered. The Pipe Replacement Decision Framework in Figure 2 depicts areas that represent varying degrees of costs, recovery time, and risk for the project types in Figure 1.

The Pipe Replacement Decision Framework in Figure 2 depicts areas that represent varying degrees of costs, recovery time, and risk for the project types in Figure 1.

Project types in the Pipe Replacement Decision Framework present risks that are the product of both the likelihood of being unable to sufficiently recover capital and the amount of capital exposed. The further investment decisions move away from the short payback and minimum expenditure programs, the closer decisions are framed by a “risk envelope” space depicted in the Framework. Trade-offs may begin to appear between lower cost pipe segments that have longer time horizons to recover capital (new branch lines with few customers) and larger capital investments with shorter paybacks (removal and replacements of entire mains in established and densely served areas). As undepreciated investments approach economic planning horizons or any other mandated useful lives, the potential for customer rate shock as obsolete capital is recovered or loss to shareholders from stranded cost presents an opportunity to look for innovative capital investment and recovery methods.

Decarbonization policies are likely to change the risk analysis. Environmental considerations may accelerate technological improvements toward lower carbon natural gas through targeted investments and state or provincial carbon intensity limits. While mandates and subsidies are by their nature distortive, they can also spur new delivery models. Power supply renewables, for example, are following a discernible cost decline as mandated investments lead to economies of scale.

Risk introduces elements of time-sensitive paybacks to traditional decision-making metrics like net present value, rates of return, and size of rate base. This may present more realistic prospects for pipe recovery for a gas company facing more ambitious decarbonization policies. The new investment decision framework should incorporate uncertainty. Decarbonization policy, the economics of electrification, customers’ preference to continue to use natural gas, and new safety protocols all change the investment views on how long new pipe will be needed.

Responses to Some Common Questions

Should the LDC continue, accelerate, or reprioritize its pipe replacement program?

Under the Pipe Replacement Decision Framework, the degree of decarbonization will be a significant driver of the answer to this question, with “net zero carbon” scenarios presenting the greatest risk, as will the timeline for phasing in the program. Pipe system integrity is regulated by the states, and federally by the Pipeline and Hazardous Materials Safety Administration (PHMSA) under the Distribution Integrity Management Program (DIMP). Given the duty to maintain a safe system, any decarbonization policy would need to support system safety to the extent the system or certain segments or subsystems remain in service. While an argument might be made for repairing, rather than replacing, the classes of leak-prone pipe (LPP) currently targeted under DIMPs, the trade-off would require careful risk analysis of the LPP in order to ensure that leaks are maintained on the system at a manageable level. Pipe replacement is usually triggered by integrity concerns or capacity needs. These investment decisions could be broadened to reflect decarbonization policies. Depending on the type of decarbonization policy adopted by the state, pipe programs may be reconfigured to include the consideration of the use of new technologies, including, for example, the use of geothermal district heating as an alternative to replacement of LPP lines.

If regulators place shareholders at risk for new pipe by ruling against stranded cost recovery, how can local LDCs manage that risk?

A significant driver of the answer to this question will depend on the carbon scenarios mandated. Investment strategy will reflect the level of increased risk and the pace of decarbonization. Asset management and portfolios, market position, and performance metrics will shift in the LDC company space. Pipe investment moves from a series of cost of service approval exercises to a dynamic consideration of available alternatives, where market forces truncate useful lives, and the probabilities change once large investments are made.

For example, changes in public policy resulting in stranded costs would raise the business risk of the company and likely merit a higher allowed return. The degree of the decarbonization under new mandates would drive whether system investment strategy would change. To the extent that gas will still be needed for generation to balance higher levels of renewables that support decarbonization, for example, investment decisions may shift to supporting new generation rather than expanding residential service. If the decarbonization policy allows offsets, then investments could be made to support the offsets (e.g., reforestation programs) to maintain a status quo business plan in regulated operations. Should renewable natural gas (RNG) be available and competitive at scale and fall within the decarbonization policies, then a company could make investments to transition to RNG supplies.

Should the company propose a change to depreciation rates for existing or new pipe?

Near-term increases in depreciation rates present ways to balance investment recovery with policy goals in an incremental manner and can be adjusted through a rate case, with due consideration to rate impacts. Future earnings levels could be relatively lower if decarbonization policy reduces rate base. For this reason, any change to depreciation or capital recovery must be made in concert with other variables such as rates of return, salvage costs, capital budgeting, or risk management. Higher depreciation rates would present a way to hedge some of the risk associated with the underutilization or early retirement of pipe. Should the type of decarbonization policy adopted lead to an early abandonment of pipe, then increasing the rate of depreciation would allow for the accelerated recovery of the investment, mitigating the risk of stranded assets.

All views expressed by the authors are solely the authors’ current views and do not reflect the views of Concentric Energy Advisors, Inc., its affiliates, subsidiaries, or related companies. The authors’ views are based upon information the authors consider reliable. However, neither Concentric Energy Advisors, Inc., nor its affiliates, subsidiaries, and related companies warrant the information’s completeness or accuracy, and it should not be relied upon as such.